Looking for a tax free, no risk investment with a guaranteed 6-18% return? This might sound too good to be true but it’s not. Once you have an emergency cash reserve it’s time to start thinking seriously about your investing strategy. Part of that strategy is finding the investment that will yield the highest return with the lowest risk. Tax considerations must also play a role when you start looking for places to put your money. If you could find a place to make a guaranteed, zero risk, tax free investment would you jump at the chance to put your money there?

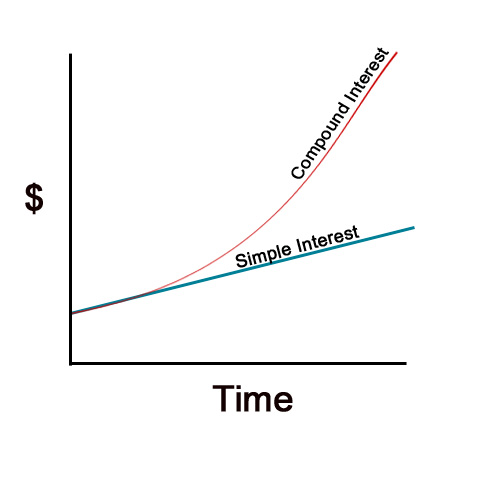

If you have consumer debt on credit cards you qualify for this “opportunity”. Your credit debt and interest payments work against any positive interest you might be accruing. Lets say you’re earning 12% a year in the stock market. After taxes you’re only getting 9% unless you’re protected by a ROTH IRA. A 9% return is the average stock market return over thirty years (minus taxes). If you have an equal amount of money in consumer credit card debt and your paying 18% a year in payments you are still down. You are actually losing -9% a year with your current investment strategy.

Risk is a considerable factor as well. If the market is down you could be earning nothing or have negative returns in the short term. This would decrease your -9% to -18% in a hurry. If you tack on inflation you’re investment strategy is negative over -20 percent!

Paying off credit cards isn’t very exciting. It doesn’t feel the same as making new money. When you add up all the positive returns you are making and subtract your negative interest it only makes sense to stop the bleeding. Once you’ve got your debt under control start making positive investments.

You might consider different debt consolidation options, selling stuff, or drive a different car. All of which will help you in your investment goals.