How much is enough for retirement? These free retirement planning calculators will help you estimate how much will be enough. Each calculator is unique in what inputs are required and the type of answers you’ll get in return.

MoneyChimp ‘Simple’ Calulator

The MoneyChimp Calculator is simple and offers a quick snapshot of what your annual retirement income might look like. This is one of my preferred calculators for a rough ballpark figure on where your finances should be. It doesn’t go into depth about social security, vacations, and other more specific items. Overall it’s a great simple to use tool. Visit MoneyChimp.com

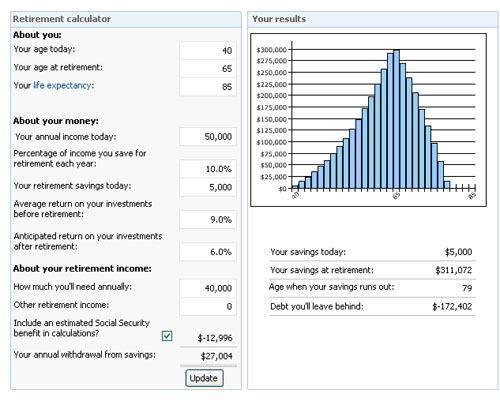

MSN Retirement Calculator

MSN’s Calculator is my favorite. It automatically updates every time you enter new information. The numbers change in the results box and the graph redraws itself. It tells you whether you’ll leave your heirs with an inheritance or a load of debt. It also informs you when you’ll run out of money. Because of the flexibility of the tool you can enter a lot of “What if?” questions and have the results instantly. One of the weaknesses of this calculator is that it doesn’t take into account inflation or yearly salary growth. Besides those weaknesses this is a very cool calculator.Visit MSN to try it out

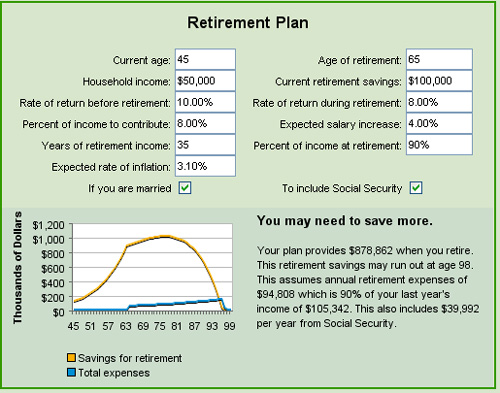

Bloomberg Retirement Calculator

Bloomberg offers a Java based calculator which is very nice if you can get it to work. It never did work on one of my computers but worked flawlessly on another. If you have a temperamental computer this calculator might not work for you. Besides that issue this calculator takes into account inflation and salary growth which is important for your final numbers. Visit Bloomberg

Things that are missing in all the calculators

None of the calculators mention ‘real dollar equivalent’, ‘relative value’, or ‘inflation adjusted’ annual income. $100,000K a year sounds pretty good right now but in the future it might be worth less, a lot less. For example, $100,000 today was only worth $20,000 in 1972 in relative value. If you planned to take home $100,000/year when you retired in 2007 it would only be worth $20,000 in 1972 relatively.

What this means is $100,000 isn’t a $100,000 in the future. 35 years from now what you know as a $100,000 might only buy $20,000 of goods and services in 2043. In other words, 1 dollar in the future might only be worth 0.20 cents in relative terms in the future. So don’t get too excited about a retirement income of $100,000 annually. There’s a good chance it might only be worth $20,000 in the future.

What does this mean for your retirement goals? It means you’ll need more than you think (especially if inflation increases like it has for the last 30 years). The way to find out how much more you’ll need is by using this tool at measuringworth.com. Take the number for your annual or monthly income from the calculators above and enter it into the ‘Initial Amount’ field. Type ‘2007’ into the ‘Initial Year’ box. Now subtract how many years you have until retirement from the current year and use that in the ‘desired year’ box. Now click ‘calculate’ and see what your money might be worth in 2043. This method isn’t a perfect prediction but it will give you an idea of what a dollar will buy 30 years from now. Visit Measuringworth.com

Wow. That was depressing. But with compound interest on your side you have a solid chance at reaching your goals. All this means is that you’ll need to start today and invest more than the minimum.

If you have any additional input on retirement calculators please leave a comment.